- Pick No-Load Funds:

Don’t pay a load. Loads, or sales fees, come straight out of your investment. There’s no evidence that load funds perform any better than no-load funds, so keep your money and stick with the no-loads (No sales charges, front loads, contingent deferred sales loads, and/or level loads). You want to make sure that you are not paying any sales charges. Sales charges come in various stripes, also known as loads or commissions. There might be a charge for buying into the fund (a front-end load) or selling the fund (back-end load, deferred sales charge, or redemption fee). Avoid all of these. Some funds have back-end loads that are reduced the longer you hold the fund. It is best to avoid these as well. If you have to buy an actively managed fund, buy the fund with no sales charges at all. Funds that normally have sales charges sometimes waive them or have reduced sales charges for large 401(k) accounts.

‘ -

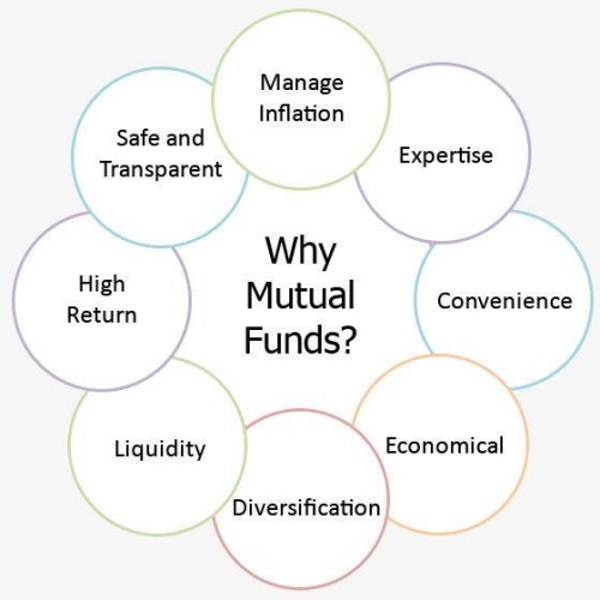

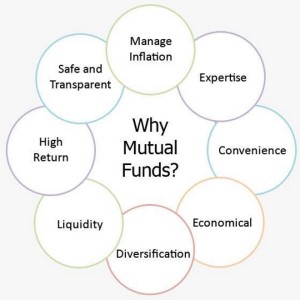

Why Invest In Mutual Funds?

A low expense ratio:

This is usually at or below 1.20%. Expense ratios represent the annual fees charged by all funds, including the management fee, the administrative costs, 12b-1 distribution fees, and other operating expenses. You want to make sure that the fees are as low as possible. Index funds typically charge about 0.20% of the assets, and actively managed funds currently average about 1.5% per year. The average fee, by the way, has actually been climbing in recent years. Any fund that has fees above 1.20% per year can be expected to under perform the total returns offered by an index fund.

‘ - Low turnover:

No higher than 45% a year, and preferably closer to 30%. Turnover measures how long a fund holds on to the stocks it buys. The longer a mutual fund holds on to a stock and the less trading the fund does, the lower the turnover will be. Since a fund incurs costs every time it buys and sells stocks (just like you do), the lower the turnover, the lower the transaction costs incurred by the fund — and the lower the capital gains taxes. Ideally, Fools like to see funds that practice the “buy and hold” method of investing — those funds are the most index-like. Funds that have a turnover of 100% are essentially buying a completely new set of companies every year. Turnover should ideally be substantially lower than the mutual fund average of about 65%. Index funds have turnover as low as 10%.

‘ - Select Four-Star or Five-Star Funds only:

These are funds with consistent average annual returns and have consistently outperformed their relative Indices over time—1-year, 3-year, 5-year, and the life of fund.

‘ - Don’t overlap:

Funds are themselves a diversified investment, but don’t think that owning a lot of funds means that you’ll be even more diversified. Instead, you may end up with many funds that own the same stocks. You should be able to achieve adequate diversification with as few as four or five funds that target different areas of the overall stock market.

‘ -

Before Investing In Mutual Funds.

Don’t chase performance:

Last year’s hot fund can be this year’s laggard. Making your fund choices based on recent performance has historically been a losing proposition. Look for long term histories through a variety of market conditions such as bull markets, bear markets, recessions and periods of economic growth.

‘ - Don’t trade in and out of funds:

Trying to time your investment and switching frequently between funds is pointless. You invest in funds to leave the trading up to a professional, so leave your money in your funds long enough for the portfolio managers to do their jobs.

‘ - Check out the management:

Look for long-term management. The fund managers should have been in their jobs and managing the fund for at least 5 years or more.

‘ - If you wanted to buy an Index fund then you would have:

For a fund manager to effectively manage and keep up with the investments in a fund and not mimic the up and down trends and performance of an Index Fund, the fund should be manageable based on the number of holdings. There should be no more than 200 stocks, bonds, or other investments in the fund, and preferably closer to 100.

‘ - Solid Track Record (as measured by consistency of the fund’s returns over time):

A mutual fund that has an established track record is less important than you would think. Studies show that measuring performance over two decades or longer, 99% of funds that outperform the market in one decade revert to the mean in the next decade. Past performance really isn’t an indication of future results. If a fund has outperformed the S&P 500 recently, determine how it does against similar Morningstar style box funds. Make sure to check out the consistency of the fund’s returns. You are looking for funds that not only have shown good returns on the whole, but ones that do so on a consistent basis, rather than having great runs followed by lousy ones. Most funds that claim to have outperformed the market over a ten-year period really had most or all of their truly good performance when they were young and small. Once the fund has attracted a couple of billion extra dollars, the fund usually starts performing more in line with the market.

‘